“How much debt is too much in India?”- Is this question disturbing? Well, if you are planning to take loans or you are already in debt then you should make an informed choice when it comes to money.

As an Indian girl, I feel that if you are not able to save a single rupee after paying off the interest on your debt every month then this is too much debt. If you are losing your sleep due to debt then you are carrying too much loan.

There are many other warning signs to say how much debt id too much in India. In this current blog, I’ll make you aware of all the things so that you should be able to avoid too much debt.

How Much Debt is Too Much in India? – AVOID DEBT TRAP

One can not say exactly how much debt is too much in India. Every person’s financial situations are different. So this depends on the loans, interest rate and most importantly on the monthly income of a person.

19 EASY Ways to Figure Out How Much Debt is Too Much in India?

Here I’m going to list out warning signs that indicate too much debt. So you should consider these important factors if you planning you take debts or if you have already taken loans in India.

1. Indian Students Borrow TOO MUCH MONEY for Education

I still remember that some of my friends had taken education loans for higher education. But I say big ‘no’ for education loans. If at all you want to apply for a student loan then you should plan your career very well to earn more money.

As per my experience and observation, unemployment and underemployment are more in India. I’ve seen that many students have taken loans but they are not getting high paying jobs. You should take a loan only if you can pay off student loan within your first year’s salary.

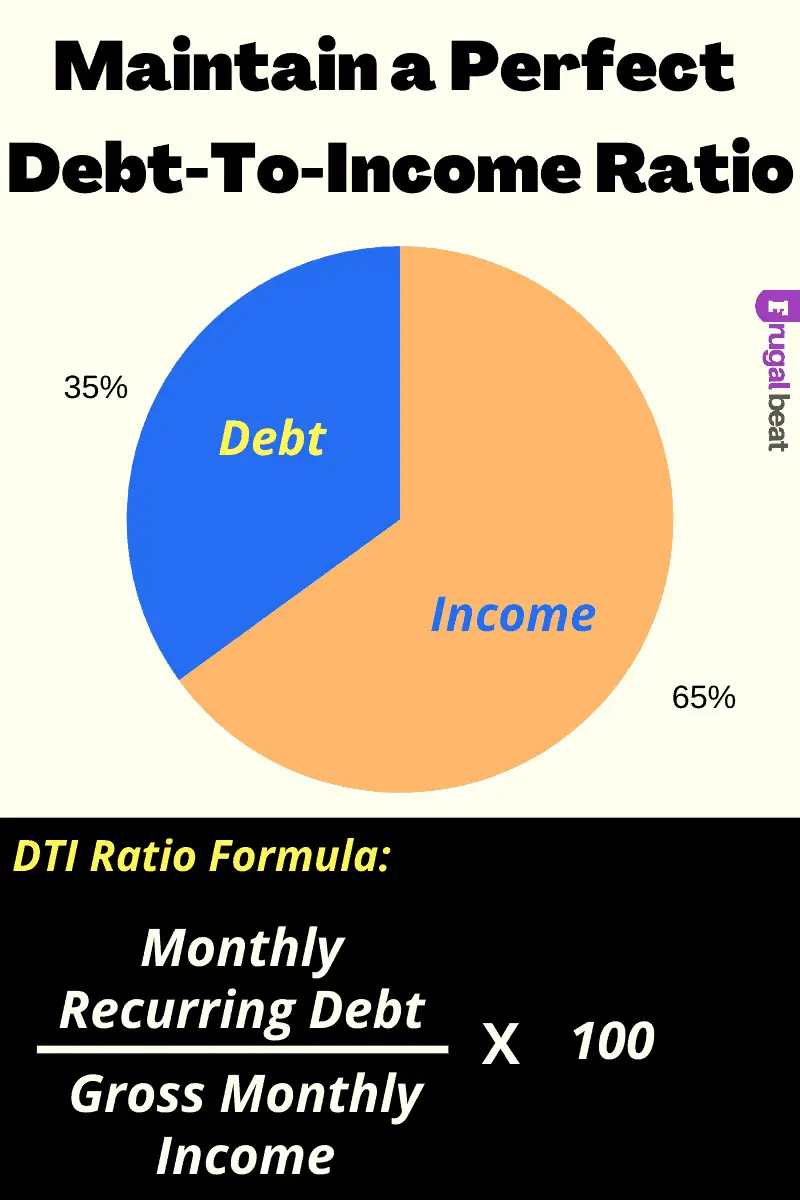

2. If your DTI ratio is more than 35% you are carrying too much debt

DTI stands for the debt-to-income ratio. This is the simple ratio between your debt and income. To maintain the perfect ratio you should either have less debt or you should try to earn extra income.

The formula to calculate DTI is recurring monthly debt divided by gross monthly income. After converting this into a percentage, f this results in more than 35% of then your debt is too much.

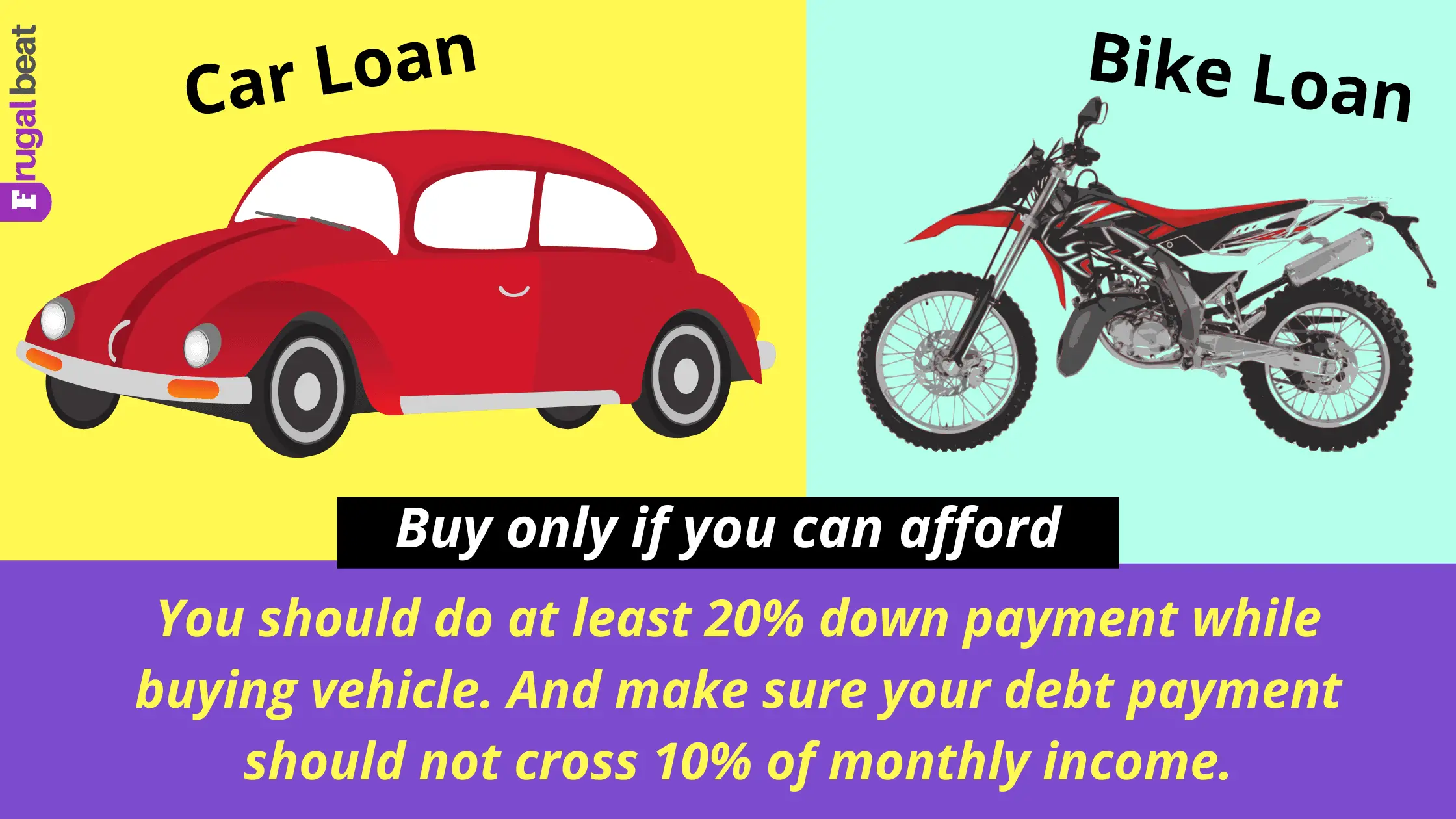

3. Know How Much VEHICLE LOAN is Too Much

Due to peer pressure, many Indians plan to have their own car or bike. Especially you can see this peer pressure in Indian youngsters. But one should not buy a vehicle if one can’t afford it. Still, people choose vehicle loans to buy a vehicle.

Here you must remember that if at all you can’t opt for a 20% down payment for the vehicle then it’s not the right time to buy a vehicle. And if you can your monthly repayment should not cross 10% of your income. Also, you should be able to pay off the whole amount within 5 years.

4. Dangerous Housing Loans to Build Your Dream House

Almost every Indian dream to have one’s own house instead of a rental house. And people opt for housing loans to buy or build a dream house.

If you want to buy a house then it is always good to check that cost should not be more than 2.5 times your annual income. And here also you should be able to pay a 20% down payment. Make sure your monthly payment should not exceed 28% of your monthly income from all the sources.

5. Taking a PERSONAL LOAN for a grand wedding

Indian wedding is like a celebration of a festival. I can understand that this is a special occasion but taking loans for a grand wedding not actually necessary.

And if at all you want to take debt for a wedding then I feel that you should be able to pay off it within 2-3 years. If you are not able to pay off within 2-3 years then you should reduce the amount. Take an affordable loan.

6. Applying for a PAYDAY LOAN until the next salary kicks in

Payday loans are very costly. Payday loan means you get some part of a loan that is usually less than your salary and you promise to pay off with your next salary. I feel that taking a payday loan itself is too much debt.

In India usually, the payday loan interest is 1% per day or ranges between 40% to 60% per month. So if you take 5000 INR for 1% then daily you your interest rate is 1% until you pay off the debt. If you pay off after 30 days then your interest rate will be 30%.

7. Not able to take care of 6 months EXPENSES

Saving money is very important. It is a basic rule for saving money to saving 6 months’ expenses. Even you can call it an emergency fund. But when you are carrying debt then you can’t save a lot of money.

If you are using your emergency fund to pay off your debt and if you are not able to contribute any money for emergency funds that means you are having too much debt.

8. CREDIT CARD DEBT is more than Housing Loan

In general, a housing loan is always more than a credit card debt. As to build or buy a house one needs more money and shopping with credit card needs less money.

But if you are realising that your credit card debt is more than your housing loan, your debt is too much. You must pay attention to your shopping and do not swipe your credit card more.

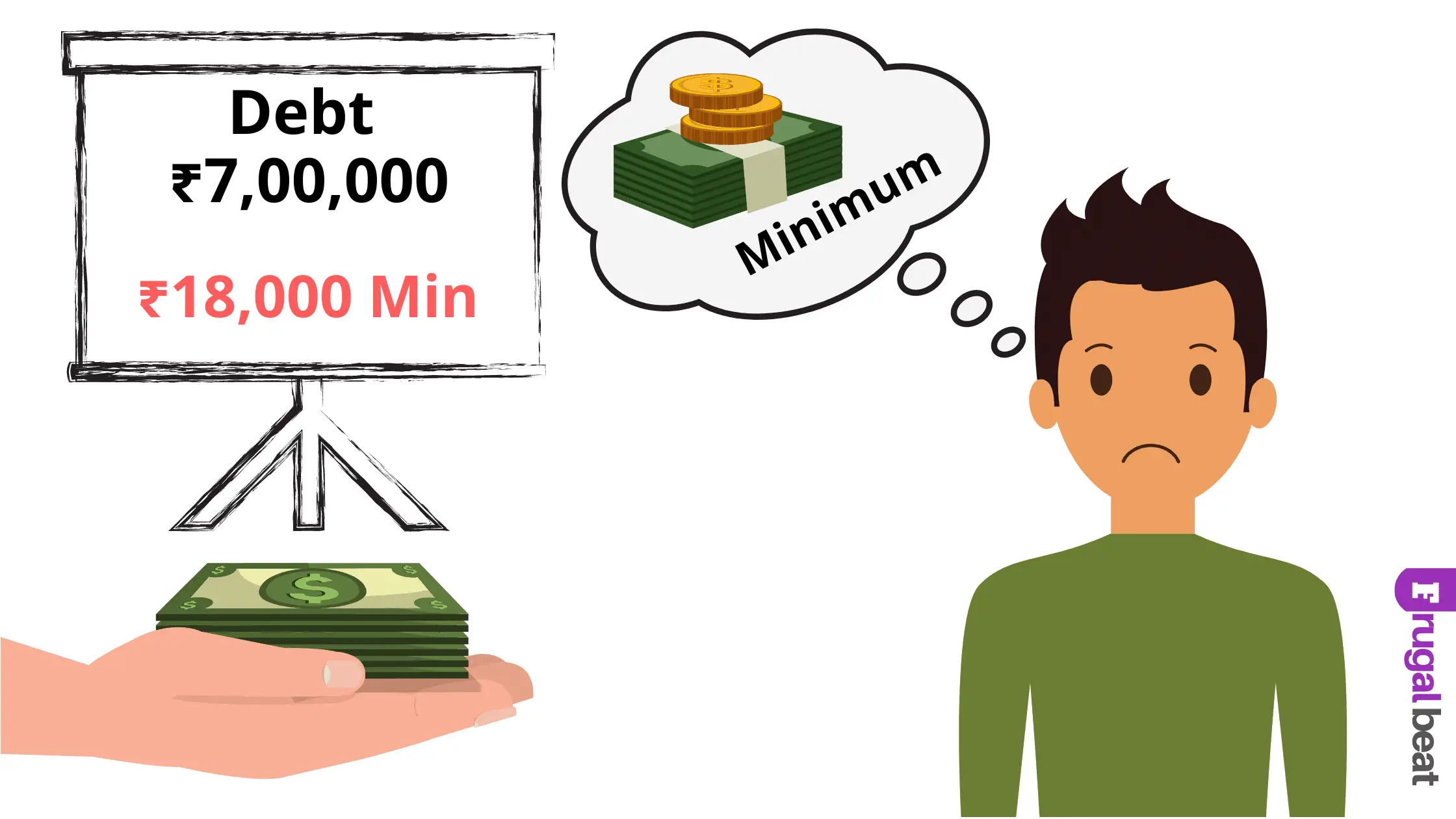

9. You make only MINUMUM payment every month

Minimum payment means paying off the only interest on the debt. If you have taken 5000 INR loans and interest is 5% then you should pay 250 INR every month to your creditor.

Also, you should try to pay some part of 5000 INR also so that your debt should be low. But if you hardly pay only a minimum amount that means your debt is too much. You are not able to pay off more than the interest rate every month.

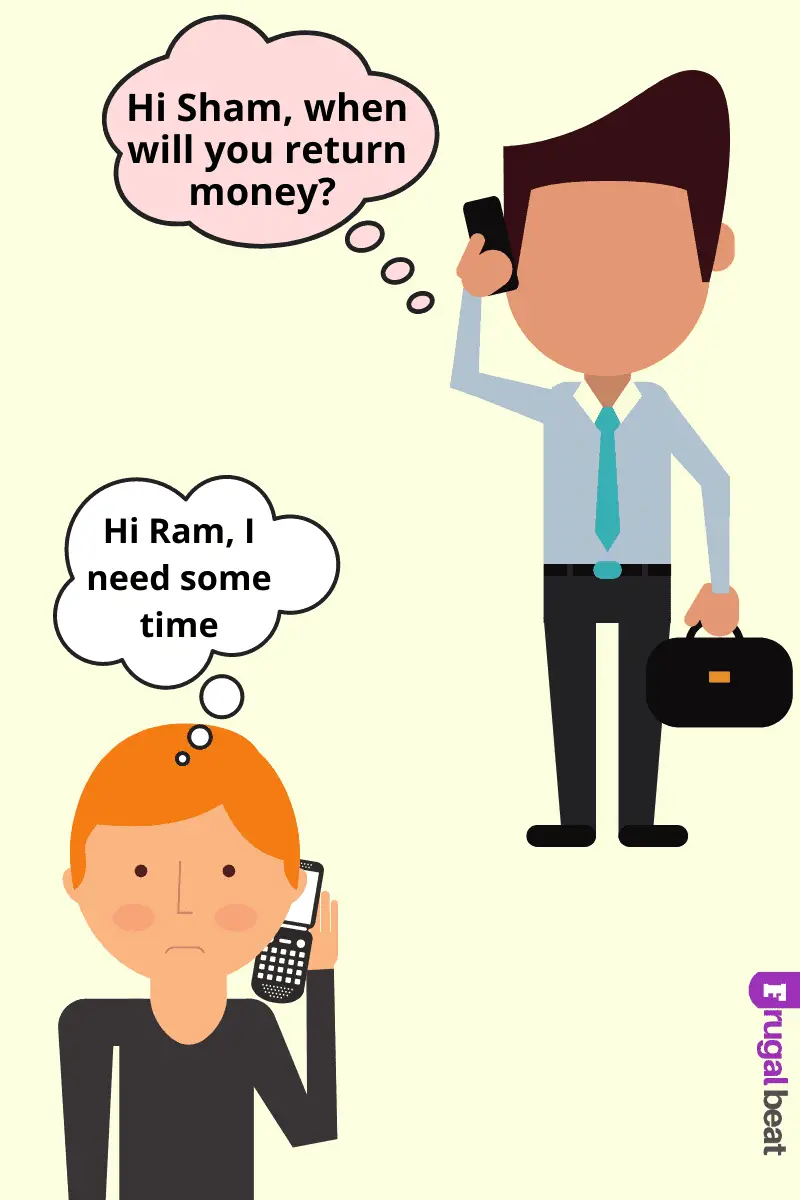

10. Creditors calling your everyday

Usually, when you check your incoming call list you find your loved ones’ name. But if you find your creditor’s name there then it is a sign of too much debt!

When you are not able to pay off your debt you get phone calls from credit agencies. That means you have taken a huge amount of loans and struggling to pay off. So always avoid taking too much debt that you can’t pay off quickly.

11. CREDIT CARDS Burn Out Your Pockets

Nowadays debit cards and credit cards are trending in India. Many youngsters are also carrying credit cards. But you should not be careful about the usage of a credit card.

Do not carry more than one credit card. If you can not pay off the credit card debt within 12 months then you are having too much credit card debt. Think twice before using your card.

12. It is a stupid idea to TAKE NEW LOANS to pay off old debts

If anyone advises you to take a new credit card to pay off old credit card debt then you should avoid this idea. Borrowing new loans to pay off the old loans will not solve your problem.

Instead, you will be having more debt. And if you are planning to borrow new debt even though if you are having old debts, you are having too much debt. So you should figure out other ways to earn money to pay off debt fast.

13. Not able to pay utility bills because of debt

The monthly repayment of debt is actually good. But at the end of every month if you are not left with money to pay for essentials and utility bill then this is not a favorable situation.

This shows that you are having too much debt that you can’t even pay monthly bills that are essential. So you should learn to pay off debt fast even if your income is low. You should learn to manage your money well.

14. Selling out your house to PAY OFF DEBT is too much debt

I’ve realized that when debt is too much then people sell out valuable things like car, gold and much more to pay off debt.

And when people do not find any other hope to pay off debt then they think of selling out their own house. So if you ever felt like selling out your house to clear debts then this is too much debt.

15. You are NOT SAVING MONEY even if you get advance salary

If you are asking your boss for an advance salary to pay off debt and still if you are not able to save some part of your income, this is a warning sign of too much debt.

You should not take loans with high interest. Also, you should maintain a balance between debt and income. Otherwise, you will be having too much debt that even advance salaries will not help you to come out of your debt.

16. Credit card scores define your CREDIT STATUS

When you swipe your credit cards often but when you make a delay in repayment your credit card scores will be poor. And even some lenders check your credit card stores before lending money. And due to poor scores, you even won’t get any further loans.

That means if you have too much credit card debt then you are having poor credit card score. Ultimately this is a sign of too much debt.

17. Paying EXTRA FEES on CREDIT CARDS every time by crossing credit limit

There are some rules for using credit cards and this varies from bank to bank or financial organization. They fix some limits for credits. And if you overuse the limit then you should pay an extra fee.

If frequently you are paying fees for crossing the limit of credit you are carrying too much debt. You should be aware of your expenses do not cross the limit of using credit.

18. If you are SKIPPING YOUR PAYMENTS you have too much debt

The monthly payment for debt is required until you pay off your full debt. If you are skipping these payments because of a more debt then you are in too much debt.

You should think about repayment before taking debt. And you should have a proper strategy to pay off debt. If you go on skipping payment that means you have taken excessive loans that you can’t afford. So plan at the beginning itself.

19. Less than ZERO NET WORTH is the sign of a heavy debt

You should balance your assets and liabilities. In simple words, your loans should not be more than your assets. That means your net worth should not be negative.

If your net worth is less than zero, you are having too much debt. And this situation actually dangerous. So you should pay attention to your all the debts. You should not have more debts than your assets.

Debt Trap in India – Be Careful

Taking some debt in times of need and paying off debt quickly is considered as good. But in India, more people are getting trapped into debt. And once you get trapped into debt then it’s very difficult to be debt-free.

Taking Excessive Loans in India

I’ve seen that many youngsters in India borrow loans based on future earning plans. But in reality, there is no certainty about future earning. If you borrow money for business then there is no guarantee that your business will go well and you pay off debt.

So it is necessary that you should always have a back-up plan. You should have different plans to pay off your debt. If not then you will get trapped into debt. You try to take more loans to pay off old debt. This is a huge debt trap in India.

If you analyze all these warning signs then you will get clarity about how much debt is too much in India. Make sure you don’t get trapped into debt. A debt-free life is a happy life, so lead a happy life and be sensible when it comes to debt.